CLEVELAND-CLIFFS (CLF)·Q4 2025 Earnings Summary

Cleveland-Cliffs Stock Jumps 6% on Tariff Tailwinds Despite Q4 Revenue Miss

February 9, 2026 · by Fintool AI Agent

Cleveland-Cliffs (NYSE: CLF) reported Q4 2025 results that missed revenue expectations but beat on EPS, sending shares up 6.3% as investors focused on an improving 2026 outlook driven by tariff protections and operational improvements. The company reported revenues of $4.3 billion (down 6.4% vs. $4.6B consensus) and adjusted EPS of -$0.45 (beating -$0.62 consensus by 27%).

The bullish reaction reflects management's confidence that Q4 2025 marked the "trough in quarterly profitability," with multiple tailwinds converging in 2026: full-year benefit of 50% steel tariffs, expiration of a loss-making slab contract, continued cost reductions, and the strategic POSCO partnership.

Did Cleveland-Cliffs Beat Earnings?

Mixed results: Revenue missed while EPS beat due to lower volumes but better cost performance.

The revenue miss was driven by a $39/ton drop in average selling price due to index pricing lags and lower shipment volumes (3.8M vs. 4.0M tons in Q3). However, cost discipline delivered a better-than-expected bottom line.

Full-year 2025 results reflected a challenging year: $18.6B in revenues, adjusted EBITDA of just $37M, and a net loss of $1.4B.

How Did the Stock React?

CLF shares jumped 6.3% to $14.73 following the earnings release, outperforming the broader market.

Key stock metrics:

- Current Price: $14.73 (+6.3%)

- 52-Week Range: $5.63 - $16.70

- Market Cap: ~$8.4B

- YTD Performance: Recovering from October 2025 lows

The stock has rebounded significantly from its 52-week low of $5.63, driven by improving tariff enforcement and the Trump Administration's focus on domestic steel. The 2026 outlook appears to have given investors confidence that the worst is behind the company.

What Changed From Last Quarter?

Several key developments distinguish Q4 2025:

1. Onerous Slab Contract Expired (December 9, 2025)

- ~1.5 million net tons annually to ArcelorMittal

- Contract was directly linked to Brazilian slab export prices

- Became a negative EBITDA contributor as Brazilian slab fell to ~$440/ton while U.S. HRC rose to ~$935/ton

- Expected EBITDA benefit: ~$500 million annually from replacing low-margin slabs with higher-margin products

- Revenue improvement of ~$700 million at current HRC prices ($970/ton HRC vs $485/ton slab price)

- Impact phases in through inventory: more visible in Q2 than Q1, even more in Q3

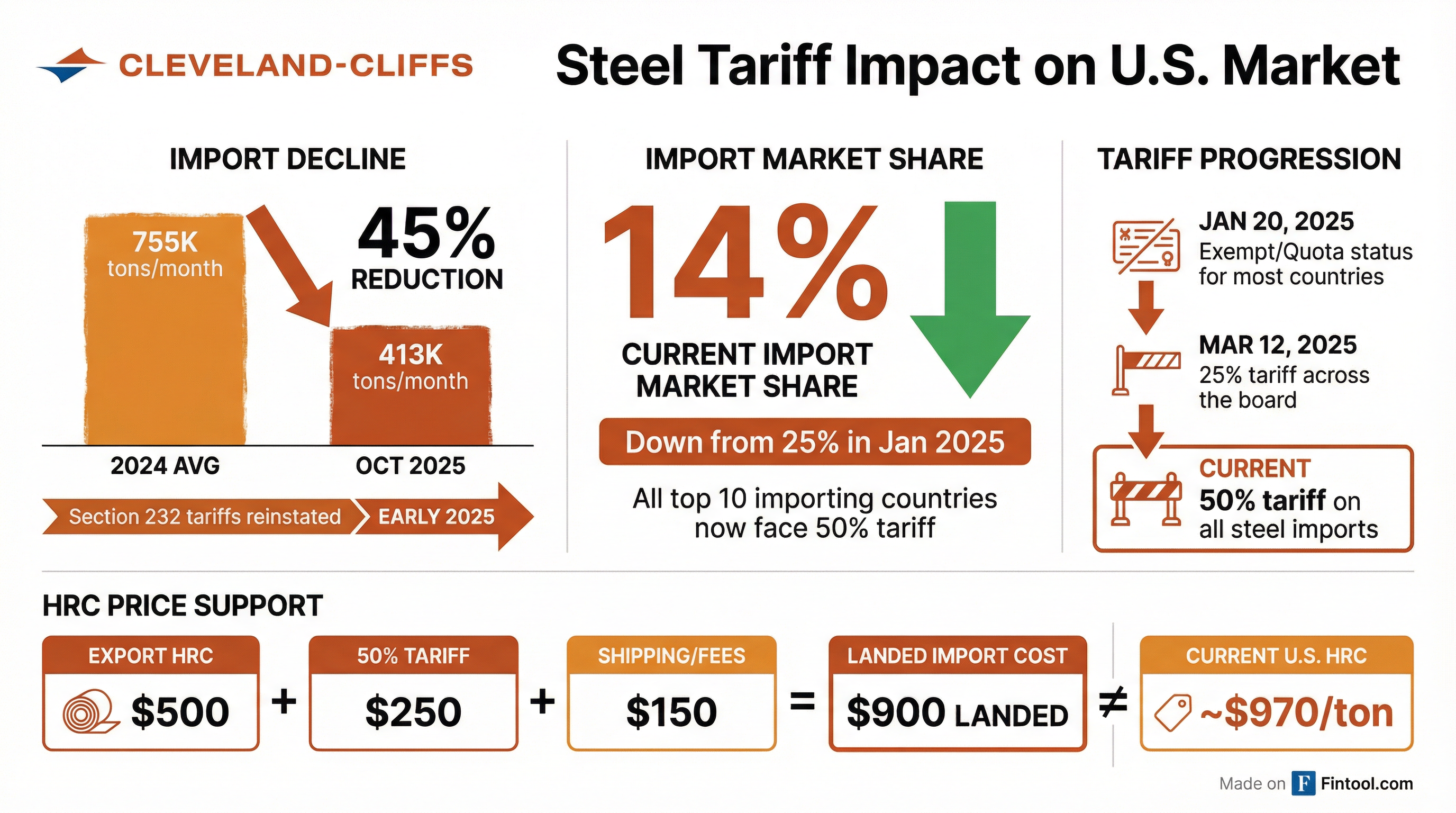

2. 50% Steel Tariffs Now in Effect

- All top 10 importing countries now face 50% tariffs (up from exempt/quota status)

- Import market share collapsed from 25% (Jan 2025) to 14% (Dec 2025)

- Flat-rolled imports down 45% year-over-year

3. POSCO Strategic Partnership

- MOU signed September 17, 2025 with Korea's largest steelmaker (world's 3rd largest ex-China)

- POSCO approached Cliffs (not the other way around) — seeking U.S. market access and melted & poured compliance

- Targeting definitive agreement in H1 2026

- POSCO still conducting due diligence; Cliffs has completed theirs

- Board will only approve if deal is accretive to shareholders

- UBS acting as financial advisor

- Larger asset sales (Toledo HBI, FPT) on hold pending POSCO outcome

4. Aluminum-to-Steel Breakthrough

- Successfully replaced aluminum with steel in automotive stamping equipment

- Moved from trial phase to routine production at three different OEMs

- Now producing parts for the "best-selling vehicle in the United States" (likely F-150)

- Steel advantages: lower cost, stronger, easier to repair, ~4x lower CO2 emissions

5. Stelco Turnaround

- Canadian subsidiary now contributing positively after disappointing 2025

- Canadian government implemented import restrictions late Q4 2025

- Canadian pricing and shipments improved significantly in recent weeks

What Did Management Guide?

Management provided explicit 2026 guidance reflecting significantly improved expectations:

Q1 2026 Specific Outlook:

- Shipments returning to ~4 million tons (up from 3.8M in Q4)

- ASP expected up $60/ton from Q4 (driven by lagging index pricing turning positive, improved Canadian pricing, higher automotive mix)

- Costs temporarily up ~$20/ton due to utility spike and mix shift, normalizing in Q2

- New pricing mix: 35-40% annual fixed-price contracts, 25% CRU month lag, 10% CRU quarter lag, 25-30% spot/other

Multi-Year CapEx Trajectory:

- 2026: ~$700M (normalized maintenance + Burns Harbor pre-work)

- 2027: ~$900M (Burns Harbor Furnace C Reline)

- 2028: Back to ~$700M

Key 2026 tailwinds vs. 2025:

- Full-year of 50% steel tariffs (vs. lagged implementation in 2025)

- No onerous slab contract dragging on EBITDA

- Market share gains in automotive

- Lower coal pricing

- Tariff-rate quota system in place for Canadian steel

The implied message: 2025 was an unusually difficult year that won't repeat.

Capital Allocation & Balance Sheet

Cleveland-Cliffs continues to prioritize debt reduction:

- Debt reduction is #1 priority — 100% of asset sale proceeds going to debt paydown

- Asset sales:

$425M expected from idled assets ($60M already received, FPT Florida closed, several under binding contract) - Additional upside: Toledo HBI and FPT assets could generate proceeds beyond the $425M, currently on hold for POSCO talks

- Pension/OPEB liabilities reduced 93% since 2020 (from $4.2B to $299M)

Capex discipline continues: 2025 spending of $561M was well below original $700M guidance, down from over $1B pro forma in 2022.

Operational Excellence: The company achieved its lowest safety incident rate since becoming a steel producer — TRIR of 0.8 per 200,000 hours worked (including contractors), a 43% improvement from 2021.

Historical Quarterly Performance

*Values retrieved from S&P Global

The trajectory shows Q4 2024 through Q1 2025 as the trough, with gradual improvement through 2025. Q4 2025's seasonally weak shipments and index pricing lags created another soft quarter, but the setup for 2026 appears materially better.

Key Risks and Concerns

Near-term:

- Steel price volatility remains elevated

- Automotive volumes still below historical norms

- POSCO transaction outcome and timing uncertain

Structural:

- $8B+ debt load requires sustained profitability to deleverage

- Cyclical steel industry remains vulnerable to economic downturns

- Trade policy changes could alter tariff landscape

Key Management Quotes

"If I can put a number on the gain, the EBITDA number by itself is to the order of $500 million just by replacing the slabs with higher margin... $500 million is a good number to start thinking about the gain." — Lourenco Goncalves, CEO on slab contract expiration

"Differently from our competitors currently building new steel plants or announcing plans to build steel plants, Cleveland-Cliffs has production capacity available right now. Again, Cliffs does not need to build plants to be ready in 2028, 2029, or 2030." — Lourenco Goncalves, CEO on competitive positioning

"We believe that we would be able to provide to POSCO the ability to meet US trade and origin requirements, particularly melted and poured... They will not be able to sell here without complying with that requirement." — Lourenco Goncalves, CEO on POSCO partnership value

Forward Catalysts

- POSCO Deal Closing — Targeting definitive agreement in H1 2026; final terms and accretion details expected

- Q1 2026 Results — First full quarter with expired slab contract and full tariff benefit; ASP up $60/ton expected

- Automotive Recovery — Multi-year fixed-price contracts with all major OEMs position CLF for share gains as reshoring accelerates

- Rare Earth Development — Two mining sites showing potential for critical minerals

Bottom Line

Cleveland-Cliffs delivered a mixed Q4 2025 with revenue missing but EPS beating, yet the stock rallied 6% as investors looked past the noise to a significantly improved 2026 setup. The expiration of a loss-making slab contract, full-year tariff benefits, continued cost cuts, and the POSCO strategic partnership provide multiple paths to profitability recovery. With the stock still well below its 52-week high and multiple tailwinds ahead, the question is whether management can execute on what appears to be a favorable setup.